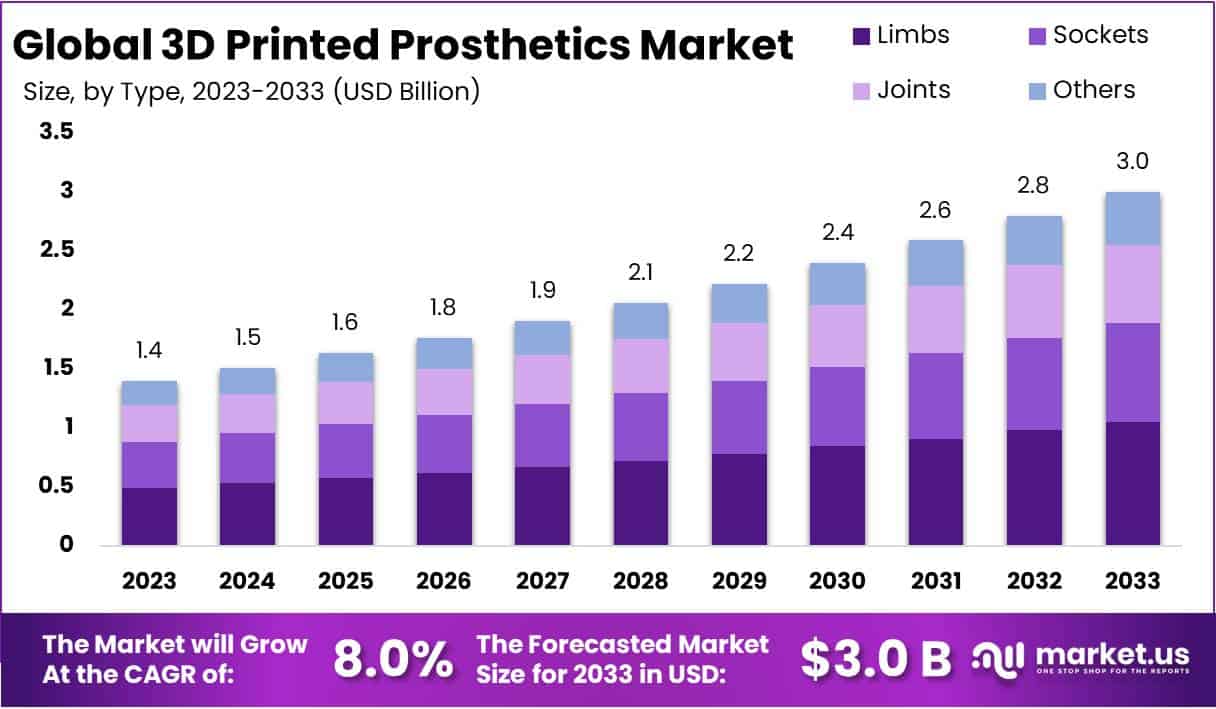

In a pivotal shift for prosthetic manufacturing, the 3D-printed prosthetics market is showing robust growth, driven by technology advances, material innovations, and changing supply-chain and reimbursement dynamics. According to a recent report from Market.us Media, the global market was valued at approximately US $1.4 billion in 2023, and is projected to reach around US $3.0 billion by 2033, representing a compound annual growth rate (CAGR) of about 8%.

Key Growth Drivers

Several converging trends are underpinning this growth:

-

Customisation & fit-accuracy: 3D scanning and additive manufacturing allow prosthetic limbs, sockets and joints to be tailored precisely to the user’s anatomy — improving comfort, wearability and performance.

-

Reduced cost / shortened timelines: Additive processes minimise material waste, reduce manual labour and allow faster iteration. Clinics and labs are increasingly adopting these workflows to improve turnaround.

-

Material & design innovation: New polymer blends, composites, lightweight structures and modular components are improving durability, flexibility and aesthetics of 3D printed prosthetics.

-

Broadening access globally: The technology is increasingly enabling point-of-care production, localised manufacturing and cost-effective solutions in emerging markets — key for regions with high unmet prosthetic need.

-

Regulatory & reimbursement progress: Advances in regulatory clarity and reimbursement pathways (for example in the U.S.) are reducing barriers to clinical adoption.

Market Segmentation & Regional Insights

-

In terms of type, the “limbs” segment (i.e., full prosthetic limbs) led in 2023, accounting for about 35.1% of global revenue.

-

By material, polypropylene was dominant in 2023, holding roughly 34.4% of the revenue share — likely due to its favourable balance of weight, strength, sterilisation compatibility and cost.

-

By end-use, hospitals were the largest sector, capturing around 41.7% of global revenue in 2023 — emphasising the importance of healthcare-institution workflows and infrastructure in prosthetic adoption.

-

Regionally, North America is the front-runner, contributing over 42% of revenue in 2023. Meanwhile, the Asia-Pacific region is forecast to show the fastest growth rate over the coming decade, driven by rising injury incidence, growing middle-income populations and investment in healthcare infrastructure.

Implications for the O&P Ecosystem & Stakeholders

For prosthetists, orthotists, manufacturers, and supply-chain partners—particularly in regions such as the Middle East, Africa and India—these findings carry several strategic implications:

-

Design & digital workflow integration: As customisation becomes the norm, clinics that invest in 3D scanning, CAD/CAM modelling and in-house or partnered additive manufacturing will be better positioned to deliver differentiated services.

-

Material sourcing and manufacturing strategy: Understanding which materials (e.g., polypropylene blends, advanced composites) and printing technologies (SLA, SLS, FDM, etc) are gaining traction helps inform procurement and manufacturing decisions.

-

Local manufacturing & supply-chain resilience: The ability to manufacture prosthetics closer to pointofcare will reduce lead‐times and logistics costs, which is especially relevant in regions with geographical or infrastructural challenges.

-

Regulatory & reimbursement awareness: As 3D-printed prosthetics gain formal reimbursement status (e.g., U.S. Medicare updates) and regulatory frameworks mature, clinics and manufacturers will need to align quality systems, validation, traceability and outcome tracking accordingly.

-

Emerging market opportunity: For O&P players in MEA (Middle East & Africa), India and beyond, the growth in emerging markets presents an opening. Affordable, custom 3D-printed prosthetics can address significant unmet demand in regions with limited access to conventional prosthetics.

-

Human-centric design & sustainability: The market commentary highlights not just custom fit, but also patient-involvement (co-design), aesthetic appeal, sustainability (recyclable/modular components) — all of which mirror your interest in digital workflows, humanitarian impact and regional manufacturing ecosystems.

Challenges & Considerations

While the outlook is positive, several constraints must be factored:

-

Skillsets & workforce readiness: Clinics and manufacturers need staff trained in digital scanning, CAD modelling, additive manufacturing processes, and post-processing workflows — there is a gap to be addressed.

-

Regulatory & quality assurance: Ensuring 3D-printed prosthetics meet relevant medical device standards (ISO, FDA or CE, etc) remains a critical step for clinical acceptance and reimbursement.

-

Material certification & long-term performance: New materials and lattice/structural designs must prove durability, biocompatibility and safety in long-term use (especially for pediatric and active users).

-

Cost-benefit and reimbursement models: Although 3D-printing reduces certain costs, clinics must articulate value (faster turnaround, better fit, fewer adjustments) and navigate reimbursement landscapes in each region.

-

Supply-chain adoption in emerging regions: Infrastructure, regulatory support, local material availability and digital workflow readiness vary widely — local implementation will require tailored strategies.

Outlook: What This Means by 2030

By 2030, we can expect the following:

-

Widespread adoption of 3D-printed prosthetic sockets and limbs as standard-of-care in many clinics, with significantly reduced lead-times and increased customization.

-

Mature in-house or near-clinic manufacturing models (digital scanner → CAD → print → post-process) being commonplace in advanced clinics.

-

Expanded access in emerging markets, thanks to localised production, lower cost designs and modular/upgradable prosthetics.

-

Greater integration with digital health: remote scanning, tele-fitting, cloud-based design libraries, and maybe modular upgrades for changing patient needs (e.g., pediatric growth, athletic demands).

-

A shift in the O&P supply chain: materials, printers, software platforms, and design services will become increasingly important as competitive differentiators.

Conclusion

The 3D printed prosthetics market is entering a phase of strategic expansion—driven by customisation, technology, cost-efficiency and global access. For the O&P sector (globally and in the MEA/India region), this offers both opportunities and responsibilities: to adopt digital manufacturing, enable localised production, build workforce capacity, navigate regulatory/reimbursement landscapes and focus on patient-centric outcomes.

.jpeg)

-1.png "Gaza Fund (1)-1")