The Indian Custom Orthotic opportunity is not just commercial; it is also strategic and clinical: to shift India from a late, surgery-dominated model of managing knee OA and foot problems toward early, biomechanically intelligent interventions—with custom foot orthoses at the center of that shift.

Flat feet combined with knee osteoarthritis is emerging as a major and under-served issue in India. Recent community data from rural South India show that over one-third of adults aged 40+ (≈35%) meet criteria for knee osteoarthritis, confirming that “one in three to one in four” adults in this age group with symptomatic OA is a realistic estimate.

When you overlay this with adult flat-foot rates reported around 10–25% in various Indian cohorts, the biomechanical case for custom foot orthoses becomes very strong.

This combination—high mechanical load at the knee, altered alignment from flat feet, and a rapidly aging population—creates a structural opportunity for the custom foot orthotic market in India, similar to what North America and Europe experienced over the last 30 years.

How North America and Europe Built Their Foot Orthotic Markets

Over the past three decades, North American and European markets have moved custom foot orthoses from a niche, specialist product to a mainstream tool in musculoskeletal and diabetic care.

-

Clinical evidence + podiatry / physio leadership

-

From the 1990s onwards, podiatrists, sports physicians and physiotherapists in the US, Canada and Europe increasingly prescribed custom orthoses for plantar fasciitis, over-pronation, sports injuries and knee OA.

-

This was supported by a growing body of biomechanical research on how insoles and wedges can reduce plantar pressures and modify knee joint loading in medial compartment osteoarthritis.

-

-

Reimbursement and diabetic care

-

In North America, insurance coverage (Medicare, private payers) for diabetic footwear and custom insoles was a major accelerator.

-

As diabetes and obesity rose, orthoses and insoles were framed not just as comfort products, but as preventive devices to reduce ulcer risk and delay surgery.

-

-

Industrialization and retail channels

-

The industry moved from artisan labs to CAD/CAM and semi-automated manufacturing, enabling consistent quality and scalable production.

-

Foot orthoses began to appear in multiple channels: hospital clinics, community podiatry, sports medicine centers, specialty retail and later e-commerce.

-

-

Market outcomes

-

Today, North America controls ≈40–43% of the global foot orthotic insoles market, with Europe the second-largest region.

-

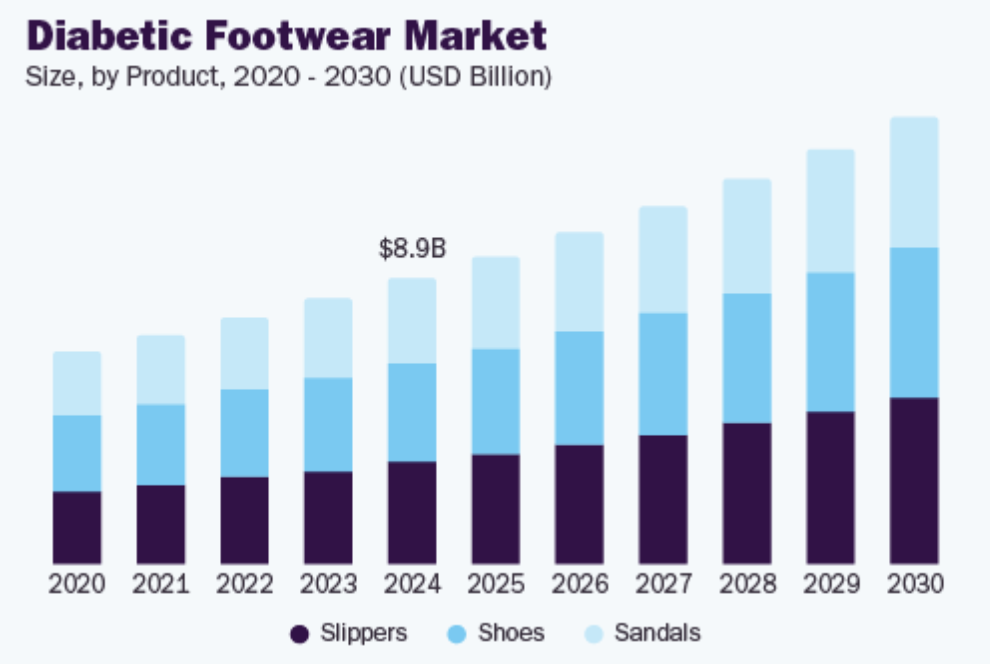

The global custom foot orthotic market is projected to grow from USD 5.2 billion in 2025 to USD 8.8 billion by 2032 (7.7% CAGR).

-

In short: North America and Europe have spent 30 years normalizing orthoses as standard of care for foot and knee problems, backed by technology, reimbursement and strong clinical advocacy.

India Today: High Need, Low Structured Supply

India is now where North America and Europe were 20–25 years ago—but with much higher population scale and an even stronger OA signal.

-

A recent community study in rural South India found a knee OA prevalence of 34.6% among adults aged 40+, with obesity, diabetes and certain lifestyle factors as key risks.

-

Systematic reviews report knee OA prevalence close to 47% in elderly Indians, highlighting a substantial burden in older age groups.

-

Adult flat-foot prevalence in Indian samples commonly falls between 11–27%, depending on age, occupation and measurement method.

Yet, custom foot orthoses in India remain:

-

Largely artisanal, fabricated by a limited number of clinics, labs and O&P centers

-

Concentrated in metros and high-end private hospitals

-

Often seen as a niche “comfort” add-on rather than a core joint-preservation and load-management tool

For many patients with flat feet and knee OA, the default pathway is analgesics, occasional physiotherapy and, eventually, joint replacement—with very little structured use of orthoses to modify biomechanics early in the disease course.

The Custom Foot Orthotic Opportunity in India

1. Clinical and demographic tailwinds

-

India has a large and growing pool of adults 40+ with symptomatic knee OA, plus a high prevalence of flatfoot and obesity in urban and semi-urban populations—exactly the profiles where custom orthoses are clinically relevant.

-

Knee pain is increasingly being reported even in people in their 30s and 40s, driven by sedentary work, weight gain and prior sports injuries—suggesting that demand will start younger than it did in many Western markets.

2. Economic and system pressures

-

Joint replacement surgeries are expensive, urban-centric and capacity-limited. Even a modest deferral of surgery age through better load management is economically attractive for both patients and payers.

-

Custom foot orthoses are relatively low-cost, low-risk interventions that can be delivered at scale if manufacturing and distribution are standardized.

3. Technology leapfrog potential

Unlike North America and Europe, which moved slowly from plaster casts to CAD/CAM, India can jump directly into digital workflows:

-

3D foot scanning via smartphones or low-cost scanners

-

Centralized CAD design and automated or semi-automated milling / 3D printing of insoles

-

Cloud-based prescription platforms linking orthopedists, physiotherapists, CPOs and central labs

This enables hub-and-spoke models, where rural or tier-2 clinics capture data and central facilities produce orthoses at scale.

Learning from 30 Years of Western Market Growth

The North American and European experience offers a clear playbook for India:

-

Position orthoses as part of joint-preservation and diabetic strategies, not just comfort

-

Integrate custom insoles into OA knee protocols and diabetic foot pathways in major hospitals.

-

-

Build clinical champions

-

Train orthopedic surgeons, physiotherapists and CPOs in evidence-based orthotic prescription for knee OA, flatfeet, plantar pain and post-injury rehab.

-

-

Standardize product tiers

-

Tiered offerings (basic, mid, premium) can address different price sensitivities while maintaining clinical logic and manufacturing efficiency.

-

-

Invest in branding + patient awareness

-

North America’s market grew because patients started asking for orthotics; India will follow once people understand that orthoses can reduce pain, delay surgery and improve daily function.

-

-

Align with payers and corporates

-

Employer health programs, joint-care packages, and eventually insurers can bundle custom orthoses into chronic disease and musculoskeletal plans, just as happened in Western markets.

-

Conclusion: A 10–15 Year Window to Build India’s Foot Orthotic Ecosystem

Globally, custom foot orthotics are a multi-billion-dollar and steadily growing category, with North America and Europe capturing most of the current value.

India, with:

-

Very high knee OA prevalence in adults 40+,

-

A sizeable and growing flat-foot and obesity burden, and

-

An underdeveloped but rapidly modernizing rehabilitation and O&P ecosystem,

represents the next major growth frontier for custom foot orthoses.